The Hidden Small Cap That Quietly Owns 75% of India's Concrete Equipment Market

Near-monopoly in concrete equipment. Pristine balance sheet. Misread by screeners.

Note Before We Begin

The single most non-obvious thing about Ajax Engineering is this: it pioneered its core product in India in 1992, has never lost market leadership since, and yet 98% of retail investors today couldn’t tell you what it makes. That invisibility is exactly why it’s worth understanding.

Hold that idea. Everything else in this article flows from it.

Hiding Inside Every Construction Site You’ve Ever Passed

Look at any construction site in India. Not the gleaming ones — the everyday ones. A road being widened somewhere outside Nagpur. A canal embankment in Chhattisgarh. A government building in Uttar Pradesh. What you’ll see, in nearly every case, is five to ten labourers crouching around a drum mixer, shoveling sand and cement and water in by eye, watching the consistency, guessing the ratio. One person adds too much sand. Another forgets to check the water-cement ratio. The output varies batch to batch. The labour cost is significant. And if you need to pour concrete at the far end of a two-kilometer irrigation channel, you’re carrying it there by hand.

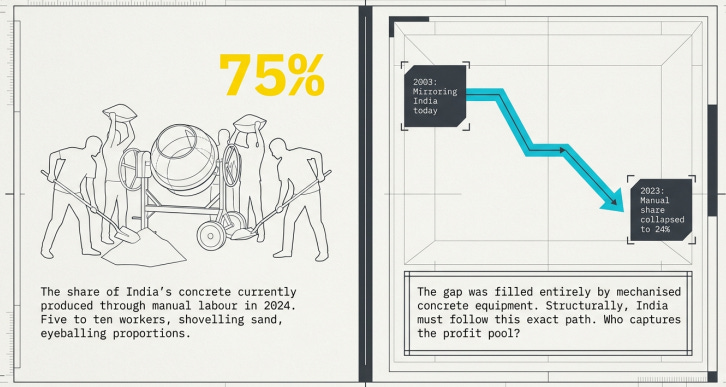

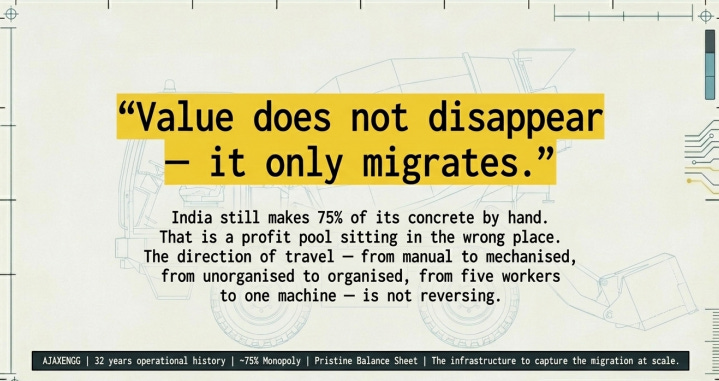

This is not a historical description. As of the most recent industry data, roughly 75% of all concrete in India is still produced exactly this way.

Now look at what China did. In 2003, China’s share of manually mixed concrete was broadly similar to where India sits today. By 2023, that share had collapsed to 24%. The gap was filled entirely by mechanised concrete equipment — machines that load their own raw materials, mix them to a precise ratio, and drive themselves to the pour point. India, as its infrastructure scales from lakhs of crores of annual government capex, is on exactly the same trajectory. The only question is who captures the profit pool as that migration happens.

“Value does not disappear — it only migrates. The question is always: to whom?”

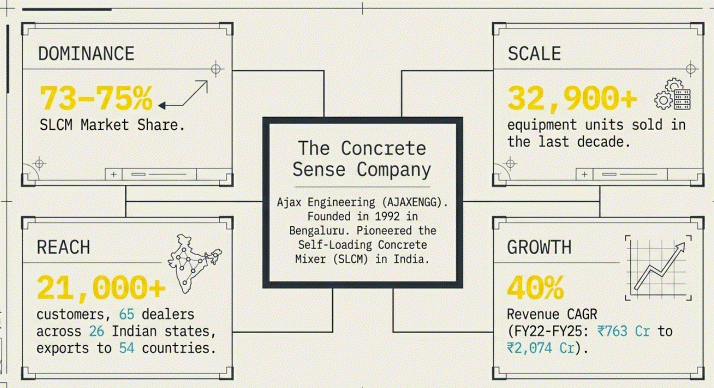

The answer — with roughly 73 to 75 per cent of the Indian self-loading concrete mixer market, zero debt, ₹810 crore in cash and investments, and a track record of profitability through demonetisation, GST, COVID-19, two election cycles, and a major emission norm transition — is Ajax Engineering Limited. It listed on the NSE and BSE in February 2025. It has been in business since 1992. And right now, for reasons that are entirely temporary and identifiable, it is trading through a margin trough that is misleading most investors about what the underlying business actually is.

The Machine Replacing the Shovel

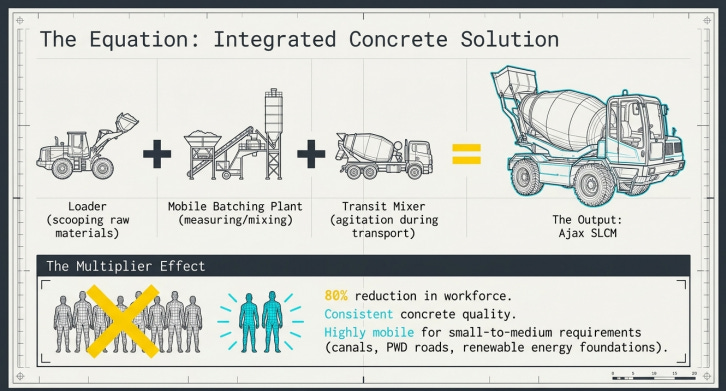

Ajax Engineering makes what is called a Self-Loading Concrete Mixer, or SLCM. If you have driven past any construction site in India, you have almost certainly seen one — a stocky, all-wheel-drive yellow vehicle with a rotating drum and a front-loading bucket, moving purposefully across mud and gravel in a way that a transit mixer never could.

The machine does something deceptively simple. It combines the functions of three separate pieces of equipment — a loader, a mobile batching plant, and a transit mixer — into a single vehicle. Two people can operate it. The same output would otherwise require five to ten labourers. The concrete quality is consistent every time, because the machine measures and mixes to a precise ratio rather than relying on a labourer’s judgement. And the machine drives itself off-road to wherever the concrete needs to go, which matters enormously for irrigation, roads, and power plant foundations in locations where trucks cannot reach.

Ajax pioneered this product in India in 1992 and has never relinquished the leadership position it built from that first-mover advantage. As of December 2025, the company has sold over 32,900 concrete equipment units in the last ten years, serves more than 21,000 customers across 26 Indian states, exports to 54 countries, and operates through 65 domestic dealers and 130 customer touchpoints. Between FY22 and FY25, revenue compounded at 40% per year, growing from ₹763 crore to ₹2,074 crore. PAT compounded at 58%.

The Structural Tailwind Most Investors Are Missing

When most investors look at construction equipment companies, they apply a single lens: is government capex going up or down? That reading is not wrong, but it misses the more powerful and durable driver — mechanisation penetration. This second driver doesn’t stop when an election cycle is unfavourable. It doesn’t pause when a state government delays contractor payments. It is structural.

Think about what happened with private sector banking in India. For two decades, value migrated from public sector banks to private sector banks. Not because lending disappeared. Because the method of doing it got better. The same migration is happening in concrete production — from manual to mechanised, from inconsistent to precise, from labour-intensive to capital-efficient.

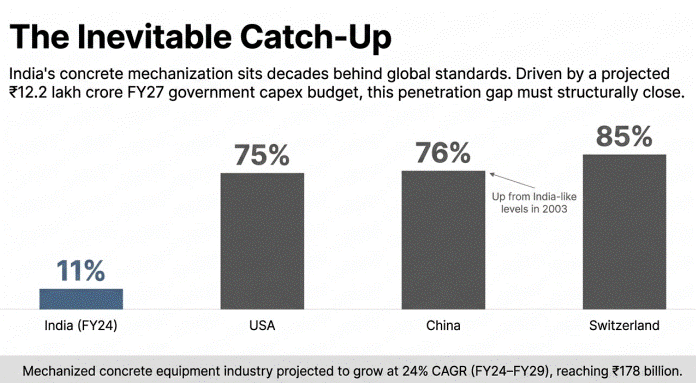

Where India Sits Today — And How Far It Has to Go

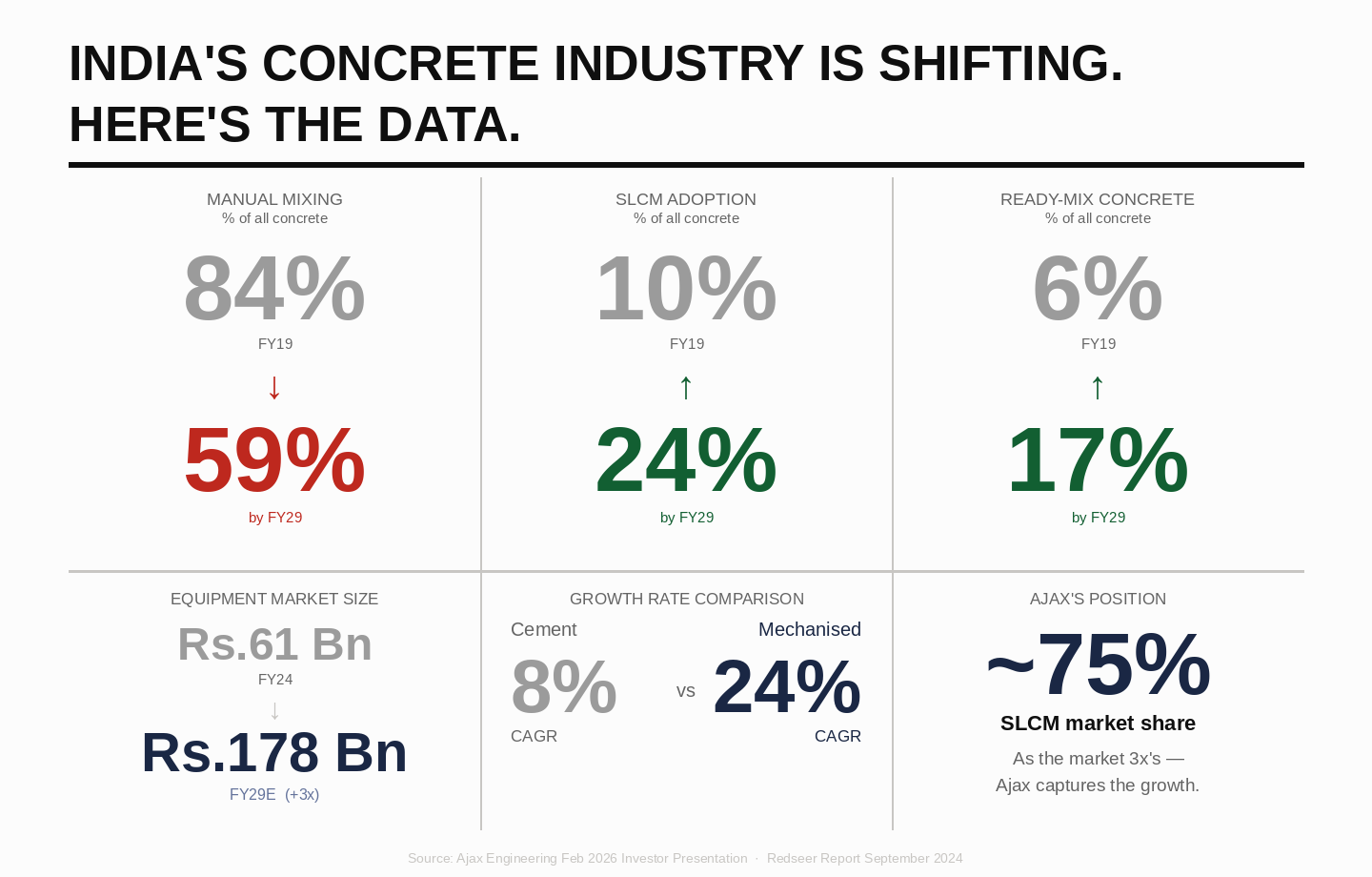

As of FY24, only 11% of India’s concrete falls into the ready-mix category — the fully mechanised form produced in batching plants and delivered by transit mixers. In the USA, that figure is 75%. In China, 76%.

India’s own historical trajectory makes the direction clear. The ready-mix share was 6% in FY19. It reached 11% by FY24. Industry projections from the Redseer Report put it at 17% by FY29. The SLCM share of concrete production followed an identical curve — from 10% in FY19 to 14% in FY24, projected to reach 24% by FY29. Manual mixing, which accounted for 84% of production in FY19, is expected to fall to 59% by FY29.

The figure that ties this directly to Ajax is the projected market size: ₹61 billion in FY24, growing to ₹178 billion by FY29 at a 24% CAGR. Ajax, with near-monopoly in SLCMs and a growing presence in batching plants, boom pumps, transit mixers, pavers, and 3D printing, is positioned to capture a disproportionate share of that incremental market value.

The Government Budget Confirms the Direction

India’s FY27 Union Budget allocated approximately ₹12.2 lakh crore for government capital expenditure — an 11% increase over FY26, confirmed by Ajax management during the Q3 FY26 earnings call in February 2026. Railways, roads, and real estate all received higher budgetary allocations. What happened in FY26 is a transmission delay — several state governments have been slow to pay contractors for completed work, and contractors waiting for payment don’t buy new equipment. This is a timing problem, not a structural break.

Ajax is one company in a much larger thesis I’ve been building around India’s infrastructure mechanisation wave. There are other sectors and themes — some with even more interesting setups than this one.

If you want them, the Small Cap Research Club is a Private Telegram community where I publish similar research reports every month. Capped at 100 members. No tips, no noise — just the same depth you just read, applied to a new business every month.

Use code ROHIT35 for 35% off.

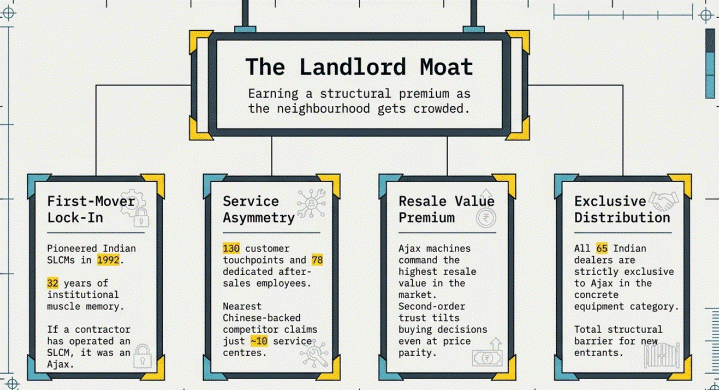

A Moat Built Over Three Decades

The competitive position here is unusual and worth understanding in some depth, because it is the kind of moat that looks simple from the outside and is deeply difficult to replicate once you understand its layers.

Why the Service Network Is the Real Barrier

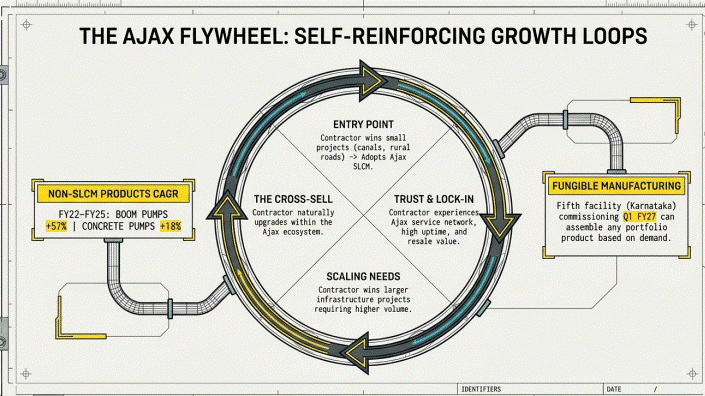

Imagine you are a contractor running a ₹35 lakh SLCM on an irrigation site in Chhattisgarh. The machine breaks down at 7am on a day when 40 workers are waiting. You need a technician on site, with the right spare part, within hours — not days. Which brand of machine do you buy next time?

Ajax has 130 customer touchpoints across 26 states, backed by 78 employees dedicated exclusively to after-sales service. Its nearest Chinese-backed competitor operates approximately 10 service centres nationally. That gap — built over 32 years, one relationship at a time — is not something a new entrant can close by writing a cheque.

First-mover institutional lock-in. Every contractor in India who has ever operated an SLCM has operated an Ajax machine. The training, the muscle memory, the spare parts that dealers carry, the resale market — all Ajax-specific. A new competitor is not selling against a machine. It is selling against three decades of embedded industry behaviour.

Highest resale value. Ajax SLCMs command the highest resale value in the Indian market per the Redseer Report. Contractors who upgrade regularly can recover more of their purchase price. That second-order trust effect tilts buying decisions toward Ajax even when a competitor offers price parity.

Exclusive dealer lock-in. All 65 of Ajax’s Indian dealers are exclusive to Ajax in the concrete equipment category. They do not carry competing brands. This is structurally unusual in capital goods distribution and makes it harder for any new entrant to build distribution reach quickly.

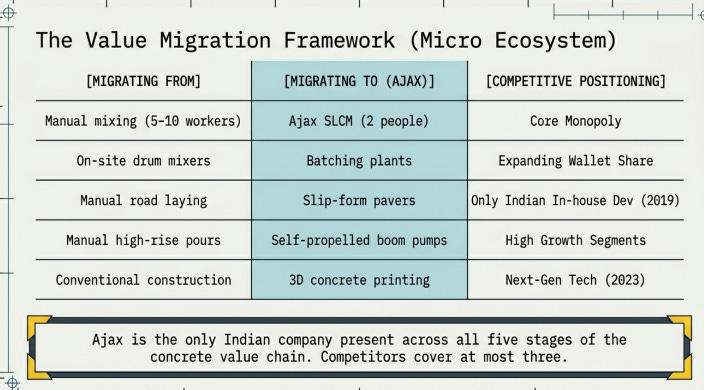

The Product Ecosystem Is Expanding

Ajax uses its 21,000-customer SLCM base as a launching pad for a complete concrete equipment ecosystem. The cross-sell logic is commercially direct. A contractor who has used Ajax SLCMs on small canal projects for five years and now wins a larger highway contract is already a warm lead for a batching plant. Ajax management confirmed in the Q3 FY26 call that SLCM customers are among the primary referral sources for non-SLCM products. Boom pump volumes grew at 57% CAGR between FY22 and FY25. Concrete pumps grew at 18%.

The fifth manufacturing facility — at Adinarayanahosahalli in Karnataka — is expected to commission in Q1 FY27. It is designed with fungible assembly capabilities, meaning it can produce any product in the portfolio based on what demand requires. That is a deliberately optionality-preserving capital decision.

Reading the Numbers Correctly.

Open any screener and two numbers will make you hesitate.

The price-to-book ratio sits at approximately 4.85 times. For a company that makes physical machines in factories, that sounds expensive — you are paying nearly five rupees for every one rupee of assets the company actually owns on paper.

But price-to-book is an accounting construct. It measures the historical cost of what a company owns. It says nothing about earning power. And earning power is everything.

Here is the simplest way to think about it. Imagine two kirana stores, both with ₹10 lakh of physical assets — shelves, fridge, counter. The first store earns ₹50,000 a year because there are four competitors on the same street. The second earns ₹3 lakh a year because it is the only shop in a two-kilometre radius. Would you pay the same price for both? Of course not. You are not buying the shelf. You are buying the monopoly.

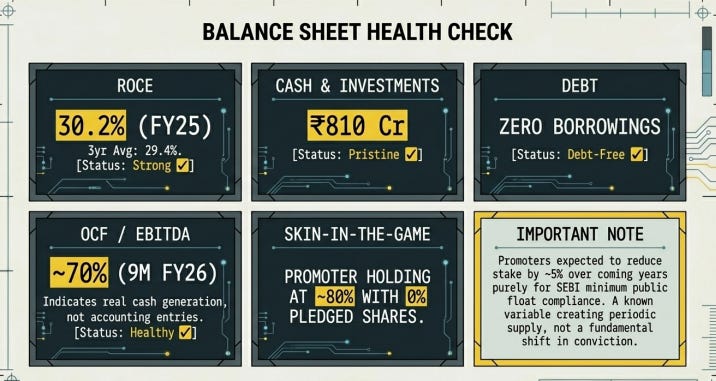

Ajax earns a Return on Capital Employed of 30.2% in FY25, with a three-year average of 29.4%. That is not a coincidence. That is what a near-monopoly in a growing market looks like in the numbers. A price-to-book of 4.85 is not expensive for a business earning 30% on every rupee it deploys. It would only be expensive if those returns were about to permanently collapse.

Which brings us to the real question worth asking — are the current margins a permanent reset or a temporary trough?

The Margins Are Down. Here Is Exactly Why.

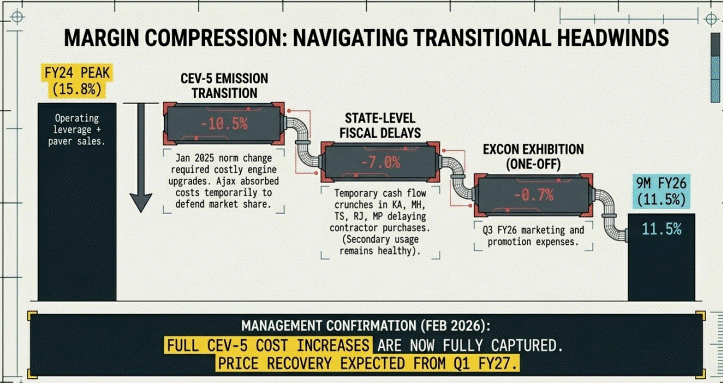

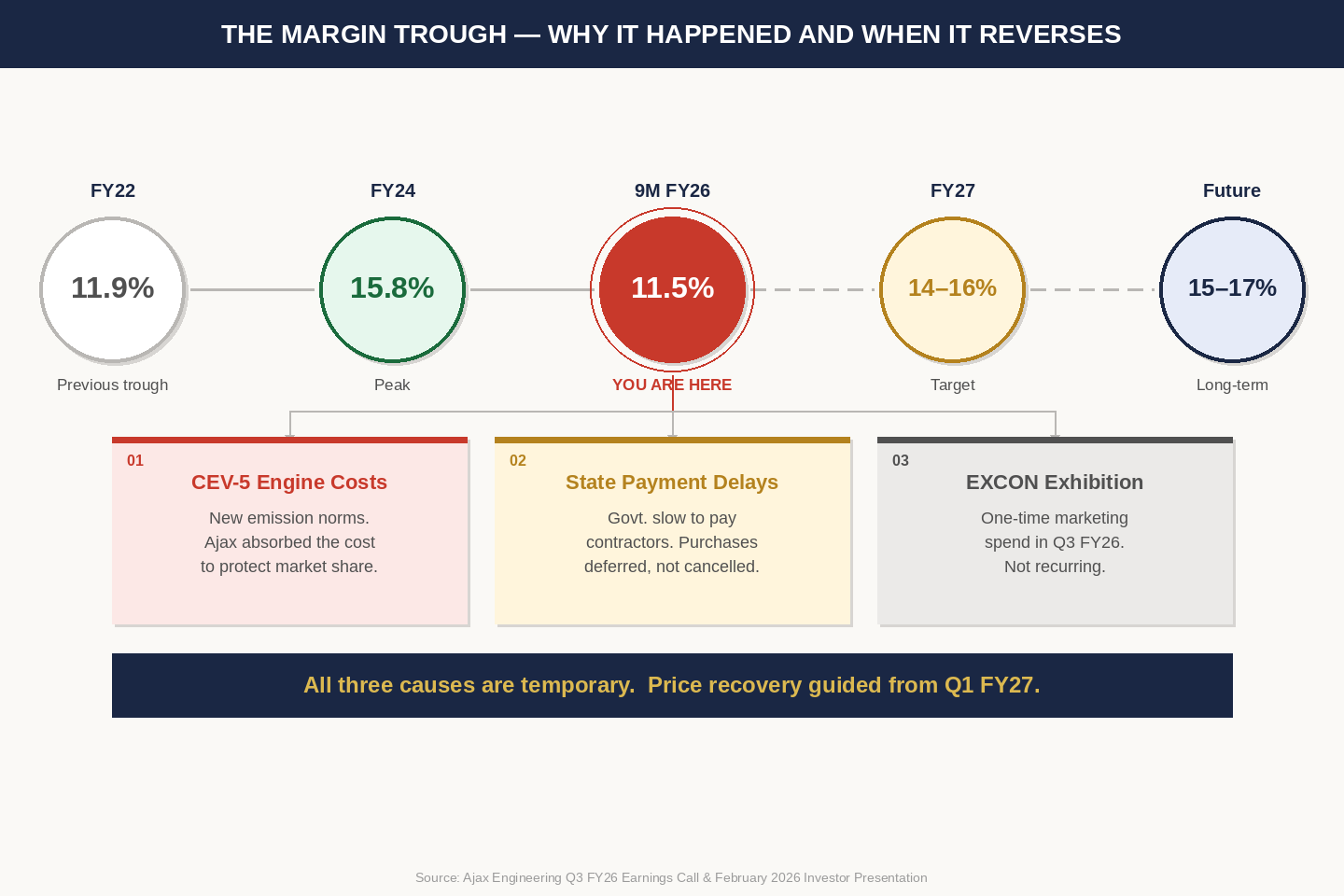

Ajax’s EBITDA margin — the percentage of revenue left after paying for raw materials, labour, and operating costs, before accounting for interest, depreciation, and taxes — peaked at 15.8% in FY24. Through the nine months ended December 2025, it sits at 11.5%.

That 4-percentage-point fall is what is creating the noise on screeners.

But before you read that number as a warning sign, you need to know what caused it. Because all three causes have names, dates, and end points.

The first cause is new engine costs that Ajax chose to absorb. From January 2025, India mandated that all construction equipment must use cleaner CEV-5 engines — the equivalent of BS6 in passenger cars. Ajax upgraded ahead of schedule, but these new engines cost more to manufacture. Rather than immediately passing that cost to customers during a soft market, Ajax absorbed it. Management confirmed in February 2026 that this cost is now fully absorbed and pricing recovery is expected from Q1 FY27.

The second cause is a payment delay — not a demand problem. Several large states — Maharashtra, Karnataka, Rajasthan — have been slow to pay contractors for completed government projects. Contractors who are waiting for payment don’t buy new machines, even when their order books are full. The clearest signal that this is a timing issue and not a demand collapse: the spare parts and service business grew 14% year-on-year in the same period. Spare parts only grow when machines are running. The machines are running.

The third cause is a one-time exhibition cost. Ajax participated in a large industry exhibition called EXCON in Q3 FY26 after a long gap. Marketing costs were one-time. Every product displayed was sold.

Three causes. All temporary. All identifiable.

The FY22 comparison is the most reassuring data point here. Ajax had an EBITDA margin of 11.9% in FY22 as it emerged from COVID. Three years later it was 15.8%. The business did not change in FY22. The context around it changed temporarily. The same logic applies today.

One Number That Tells You the Moat Is Still There

When a business is going through a rough patch, there is one number that separates a temporary trough from a permanent decline. Market share.

A company losing its competitive advantage shows up in market share first — before margins, before revenue, before anything else. Customers start quietly switching. The leading indicator turns red.

Ajax’s SLCM market share through October to January 2026 ran at 78%, 82%, 80%, and 78%. Against a long-run average of approximately 75%. During its worst margin period in three years.

The moat is not eroding. The trough is external.

The Balance Sheet Means They Can Afford to Wait

The final piece is the balance sheet — because a trough only becomes a crisis if a company cannot financially outlast it.

Ajax has virtually zero debt. Cash and investments on the balance sheet stand at ₹810 crore, confirmed by the CFO in February 2026. That is more than two and a half times the company’s annual profit sitting in cash. They are not being squeezed by this trough. They are choosing to wait it out while protecting market share, with the resources to do so comfortably.

Three numbers define this balance sheet. Zero debt. ₹810 crore in cash. And a ROCE of 30.2% — meaning the company earns ₹30 for every ₹100 it deploys. A business with those three characteristics trading at a temporary margin trough is not in trouble. It is waiting for the cycle to turn.

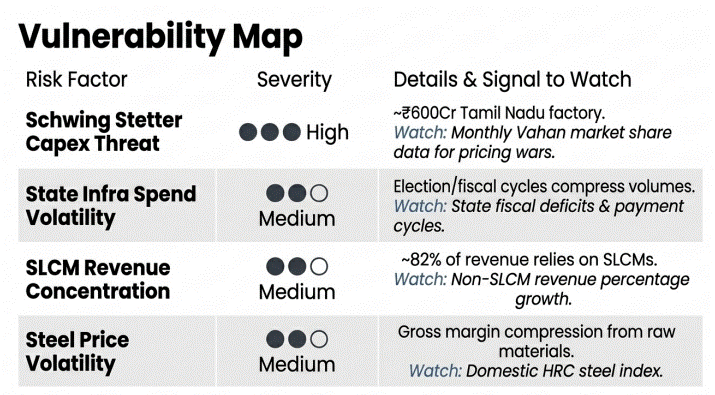

The Honest List of What Could Go Wrong

The first risk is competitive pressure from Schwing Stetter. The Chinese-owned Schwing Stetter India is reportedly investing significantly in a new Tamil Nadu manufacturing facility. If deployed aggressively in the SLCM category, it could delay Ajax’s pricing recovery and extend the margin trough. The signal to watch is monthly Vahan SLCM registration data — publicly available and near-real-time. Ajax’s management cited monthly figures of 82%, 78%, 80%, and 78% for October through January. A sustained fall below 70% would be the first structural red flag.

The second risk is state infrastructure spend volatility. The current softness in Maharashtra, Karnataka, Telangana, Rajasthan and MP is the proximate cause of FY26’s volume weakness. This is cyclical, not structural. The signal to watch is state fiscal balance data and contractor payment lag indicators.

The third risk is raw material volatility. Steel is Ajax’s primary input. Management confirmed in February 2026 that they see no significant near-term commodity price risk. But a sustained spike before pricing can compensate would compress gross margins. Watch the domestic HRC steel price index.

The fourth risk is revenue concentration. Approximately 82% of 9M FY26 revenue came from SLCMs. If SLCM demand remains soft beyond FY26, the non-SLCM portfolio — which grew 4.5% in 9M FY26 and 13% in Q3 FY26 — may not offset quickly enough. Watch non-SLCM revenue as a percentage of total each quarter.

Lower-severity risks include manufacturing geography concentration (all facilities in Karnataka) and the expected ~5% promoter stake reduction for SEBI compliance, which will create periodic supply pressure but changes nothing about the fundamental business.

The Direction of Travel

There is a particular kind of business that compounds quietly for decades while almost nobody pays attention. Pidilite spent thirty years selling adhesive paste before the market re-rated it. Astral Pipes was a sleepy plumbing manufacturer until suddenly it wasn’t. Both shared something with Ajax: a product that was small in cost relative to what it enabled, embedded deeply into customer workflows, and protected by distribution and service infrastructure that took a long time to build.

Ajax Engineering is not a glamorous story. Concrete equipment is not a dinner-table investment idea. The company makes machines that are yellow and muddy and park on construction sites in the middle of nowhere. But the business underneath that unglamorous exterior — a near-monopoly in a structurally growing product category, a pristine balance sheet, 30% ROCE, and a management team that has navigated thirty years of Indian economic cycles without ever losing market leadership — is exactly the kind of business that rewards investors who are willing to do the work to understand it.

“The current trough is real. The margin compression is real. The short-term volume softness is real. But the direction of travel — from manual to mechanised, from unorganised to organised, from five workers to one machine — that direction is not reversing.”

Do your own research. Read the Q3 FY26 concall transcript. Read the February 2026 investor presentation. Both are publicly available on BSE and Ajax’s website. Form your own conclusion. This article is not investment advice. But I hope it changed the question you were asking.

Thank you for reading this to the end. It means something.

A Note of Thanks

If you have made it this far, thank you. Writing about businesses like Ajax — unglamorous, structural, slow-burning — only matters if there are readers patient enough to actually sit with the story. Every subscriber, every share, every thoughtful comment is what keeps this corner of investing honest.

If This Is How You Like to Study Businesses, There’s More Where This Came From

This article is a small sample of the kind of research I do regularly for the Small Cap Research Club — a closed, private research community for serious investors who want to go beyond the surface.

What the Small Cap Research Club Actually Is

This is not a tips group. Every month, members receive:

1- 2 Stock of the Month reports — in-depth breakdowns of my favourite select small-cap businesses: business model, financial trajectory, competitive moat, risks, and key monitorables. The kind of research that usually takes weeks to compile independently.

One Sector Analysis report — a structured look inside a sector: the tailwinds, the structural shifts, where real opportunities tend to build over time. Context that makes individual stock research ten times more meaningful.

One Global or International Stock report — strong global businesses studied through the same rigorous lens. Expanding your investing perspective beyond India is one of the most underrated edges a retail investor can build.

Doubt-clearing sessions — live sessions and email support to connect research with actual market thinking.

No clutter. No random stock tips. Only structured, high-quality research for people who take investing seriously.

Limited to 100 Members Only

To protect research quality and maintain a focused community, enrollment is capped at 100 serious investors. Once full, it closes. The first 50 members who enroll get 35% off using code ROHIT35.

This piece took weeks to research and write. If it gave you even one useful idea, the best way to say thanks is a restack. It costs nothing and means everything for independent research like this.

Disclaimer: This article is for educational and informational purposes only and does not constitute investment advice or a recommendation to buy or sell any security. Past financial performance cited is historical and does not indicate future results. Please conduct your own due diligence and consult a SEBI-registered investment advisor before making any investment decisions.

Good work.